When did you last look at your EBITDA number and genuinely understand why it moved — not just that it moved?

Not the revenue line. Not the gross margin percentage. The actual operating profit tells you whether this business is truly building value or just generating activity.

In most mid-sized businesses I’ve worked with, the answer to that question is vague. The numbers are reviewed. The percentages are noted. But the specific, structural reasons why EBITDA is compressing — quarter after quarter — rarely get named with the clarity they deserve.

So let me name them.

The Revenue Illusion

The most common pattern I see is a business where revenue is growing and EBITDA is shrinking. The owner looks at the top line and feels good. The accountant looks at the operating profit and gets nervous. Both are right — and neither conversation is happening clearly enough.

Revenue growth without EBITDA improvement isn’t growth. It’s volume. And volume is expensive.

More orders means more people, more logistics, more credit extended, more scheme spend to sustain the momentum. If the incremental revenue isn’t coming with better margins than your base business, every rupee of growth is actually diluting your profitability. The business gets busier. The bank balance doesn’t reflect it.

This is where the first leak lives — not in a cost line, but in the assumption that more sales automatically means more profit.

The Cost That Doesn’t Show Up as a Cost

The second place EBITDA gets killed is in costs that are technically correct on the P&L but never examined as a system.

Take a building materials distributor I worked with. His gross margins looked reasonable. His EBITDA was consistently 3-4 points below where it should have been for his revenue size. When we mapped his cost structure properly, three things stood out.

His distribution cost had crept up because nobody had renegotiated logistics contracts in two years — and volume had changed significantly. His manpower cost had grown because he’d added people to solve problems that were actually process failures. And his scheme spend — the money going out to push secondary sales through the channel — had become an entitlement that nobody questioned any more.

None of these were one big decision. Each was a series of small decisions that felt reasonable in isolation. Together, they were quietly killing the operating margin.

This is what I mean by costs that don’t show up as costs. They’re in the P&L. But they’re not being managed as a portfolio — just accepted as the cost of doing business.

The Working Capital Drain Nobody Measures

The third EBITDA killer doesn’t even appear directly in the operating profit line — but it drives cash out of the business in ways that feel like profitability problems even when they aren’t.

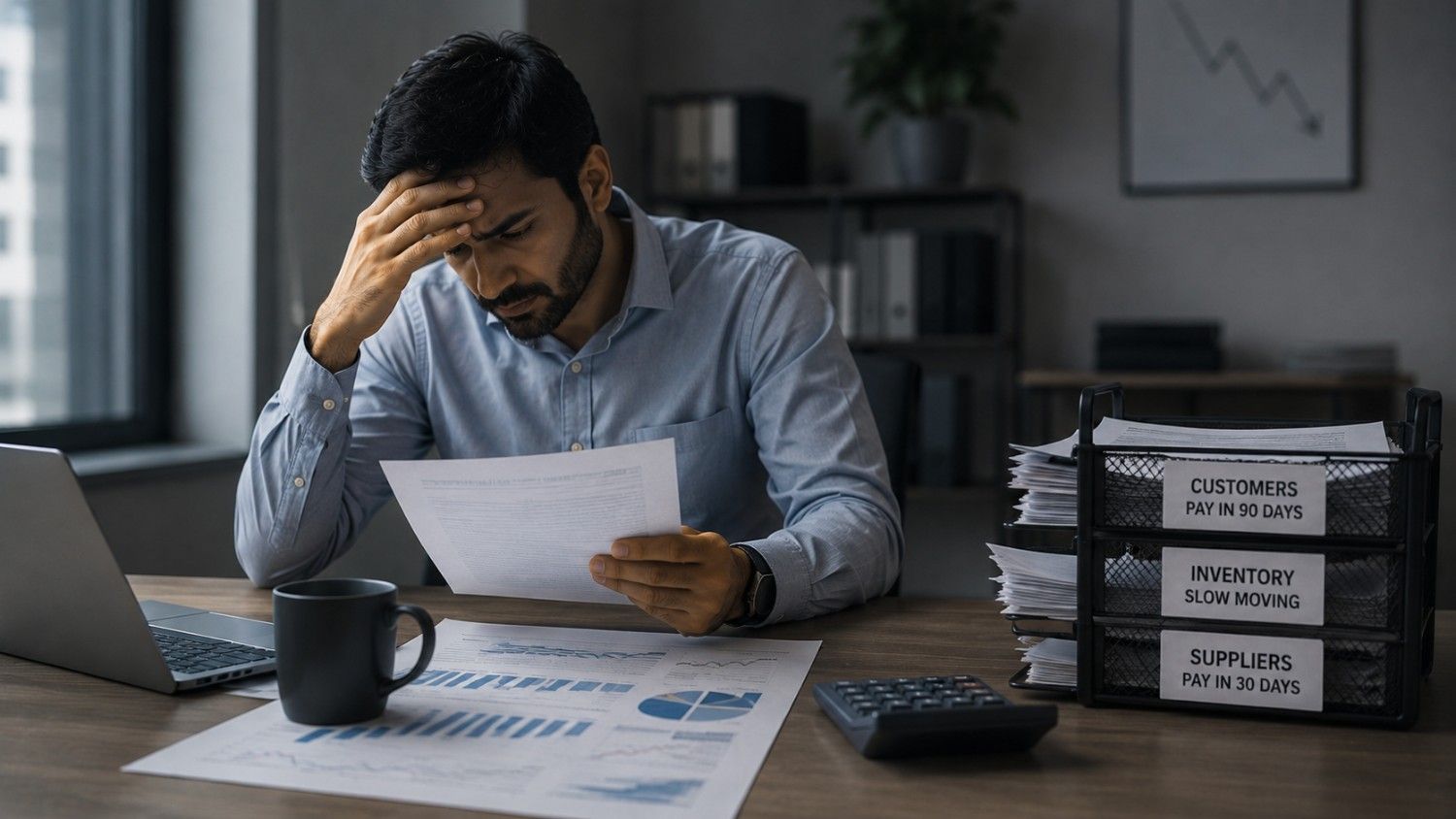

Extended credit cycles. Slow-moving inventory that was bought to hit volume targets. Debtors who are paying in 90 days while your suppliers expect payment in 30.

In an auto components business I reviewed, the EBITDA on paper looked acceptable. But the business was permanently cash-hungry. Every quarter ended with a scramble. When we looked at the working capital cycle, the picture was clear — the company was financing its customers’ operations. Credit had been extended generously for years to protect relationships, and nobody had built the discipline to pull it back.

Working capital inefficiency doesn’t kill EBITDA directly. But it forces borrowing that adds interest costs, and it creates a permanent sense of financial pressure that makes it harder to invest in the things that would actually improve the business.

The Product Mix Problem

The fourth place EBITDA shrinks is the one most owners find hardest to accept — because it lives inside what looks like success.

Your best-selling product is almost certainly not your highest-margin product. The product your sales team pushes the hardest is the one with the least friction in the conversation — and friction usually correlates with margin. High-margin products need explanation, confidence, and a salesman who believes in the value. Low-margin products sell themselves.

So over time, the product mix drifts. Volume concentrates in low-margin SKUs. The products that could move the EBITDA needle sit under-pushed, under-stocked, and under-trained on. The revenue number grows. The margin percentage falls. And nobody names it clearly because the sales team is hitting targets.

Three Questions worth Asking?

You don’t fix EBITDA compression by cutting costs blindly or pushing harder on revenue. You fix it by understanding the specific mechanism that’s causing it — and then addressing that mechanism deliberately.

→ What percentage of your revenue growth last year actually improved EBITDA — and what percentage just added overhead?

→ Which three cost lines in your P&L have grown faster than revenue over the past two years — and has anyone formally reviewed whether they should have?

→ What does your product mix look like by margin contribution — not by volume? When did you last look at that number and act on it?

EBITDA compression is rarely one dramatic problem. It’s usually four or five quiet ones operating simultaneously — each individually manageable, but collectively capable of taking a healthy business and making it feel like it’s always running just to stand still.

The businesses that fix it don’t do so with a single intervention. They do it by developing the discipline to look at the right numbers, ask the right questions, and make decisions that the P&L rewards over time — not just the revenue line in this quarter.

If your EBITDA has been under pressure and you want a clear view of where specifically it’s leaking — a structured diagnostic conversation takes 30 minutes and usually surfaces the answer. Visit-https://make10xhappen.in